What are chargebacks and retrievals?

What is a retrieval – and why do they happen?

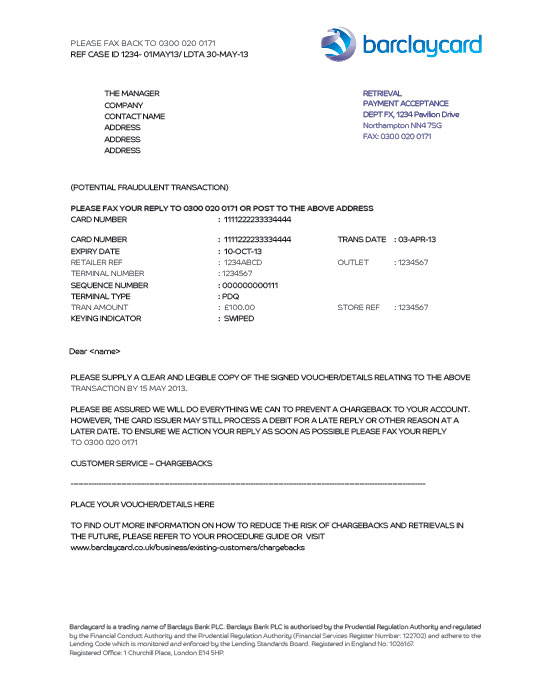

If a cardholder disputes a transaction on their statement, their card issuer will raise a ‘retrieval request’. See an example of one of our retrieval letters below.

Retrievals usually happen when your customer doesn’t recognise the payment, and is questioning whether they definitely made the payment or if the payment was fraudulent.

If I respond to the retrieval request, can a chargeback still be raised?

A retrieval request can be closely followed by a chargeback if the Card Issuing Company doesn’t receive sufficient information about the transaction in question. That’s why it’s important you send as much information as possible in your reply to the retrieval request.

Unfortunately, some retrieval requests can still lead to a chargeback even if you’ve supplied all the correct information regarding the transaction. Once the Card Issuing Company has raised a chargeback case, you’re at risk of being debited for the disputed amount.

See the chargebacks section for further information.

From your customer’s perspective, a chargeback is a reversal of a payment transaction, in an attempt to get their money back.

Chargebacks let cardholders claim back money for transactions that they or their bank feel isn’t justified.

Chargebacks can cost your business money – so it’s important to know what they are, how to respond to them and how to prevent them from happening.

A chargeback can happen for many different reasons:

These are just the most common examples – for a full list, see our page on dealing with chargebacks.

Chargebacks may also happen if your customer’s bank disputes a transaction because:

About the chargeback process

There are a couple of steps in the chargeback process:

1. Retrieval

If your customer or their bank simply wants to question what a transaction was, they can send a retrieval. The bank already has limited details of the payment like the date and amount, so you'll need to provide as much additional information as possible.

At this stage, you won't have to pay back any money. Just remember to respond to a request as soon as possible.

Sometimes this step is skipped and the claim immediately jumps to step two

2. Chargeback

If you want to dispute the chargeback, you’ll have 14 days from the date on the letter to defend it by providing evidence, depending on the reason the chargeback was raised.

An example of this would be if your customer disputed a duplicate payment, you would need to provide details showing that there were two seperate transactions.

Alternatively, if you agree with the chargeback claim, you can choose not to dispute it.

Even chargebacks that you successfully defend will ultimately cost you money or time due to the resource involved in order to defend them.

If your chargeback defence is successful at this stage and you’ve already been debited, we’ll return the funds by the same way they were taken. The time it takes to return the funds will depend on how you get billed.

Unfortunately, if you lose the chargeback appeal, you’ll be debited for the chargeback amount, plus any fees for handling the chargeback.

This debit will happen as per your previous instructions. For example, the amount could be debited to your merchant service statement, or taken by Direct Debit from your account.

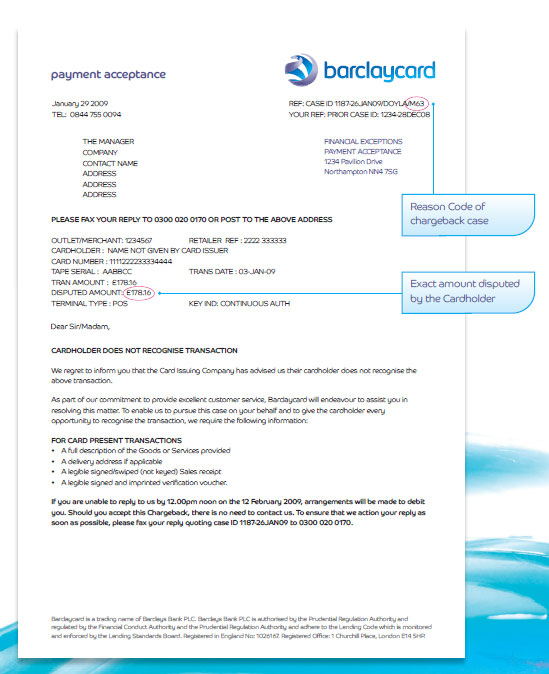

How will I know if I’ve received a chargeback?

We’ll contact you by post or fax, depending on your communications preferences (see example letter below). This will outline the evidence you’ll need to gather in order to defend the chargeback or retrieval.

In some cases, we might tell you that we’re ‘pending’ or putting the chargeback debit on hold for 14 days while we wait for a response from you.

How long do I have to respond to a retrieval/chargeback request?

You should email your response and any documentation relating to the transaction within 14 days of the date on the letter (sometimes this step is skipped, and the claim immediately jumps to step two).

For more information, visit our page on preventing chargebacks.