How can I manage my credit repayments?

Budgeting

Balance transfer credit cards can be used to simplify your credit card repayments and reduce the overall cost of borrowing.

A balance transfer is when the money owed on one credit card is transferred to another credit card. Since balance transfer credit cards usually come with a 0% interest-free introductory period, they can be a good way to pay off your debt faster.

The approval of your application depends on financial circumstances and borrowing history, so do the terms you may be offered. The balance transfer period and interest rates, may differ from those shown.

They can be especially helpful if your current credit card charges a higher rate of interest. If you keep a balance on several credit cards, it can also be a great way to tidy up your finances by moving all your credit card balances to a single card.

A balance transfer is very straight-forward. The balance from your current credit card is moved to a new credit card – so the amount owed on your old card will now appear on the new one. For example, if you transfer £2,000 from your existing credit card to a new one with a 15 month 0% interest introductory offer, you’ll have nothing to pay for the first 15 months.

After that, you’ll pay a minimum of £138 each month. This will cover your repayment on the £2,000 transfer plus the initial transfer fee, which is usually between 1% and 4% of the total amount that you transfer.

Of course, if you use your card for additional spending and don’t pay it off, your monthly payments will be higher once the introductory offer ends. So it’s important to try to pay off your balance within the offer period. Otherwise, you’ll be charged interest at regular rates on the remaining balance. You can find out more about how to get the most from these cards in our simple guide to balance transfers.

.

By avoiding higher interest rates for a limited time, balance transfers with 0% interest offers give you breathing space to pay what you actually owe rather than the monthly interest. Other balance transfer cards might still have interest, but at a lower rate than what you’re currently paying. By moving your balance, not only could you save money, you could also get that debt-free feeling sooner.

Paying credit card bills with high interest rates is tough, because most of the monthly repayments go towards paying off the interest while the debt itself takes longer to repay. But with balance transfer credit cards, your account has 0% interest for a promotional period, so you can focus repayments on reducing the outstanding balance.

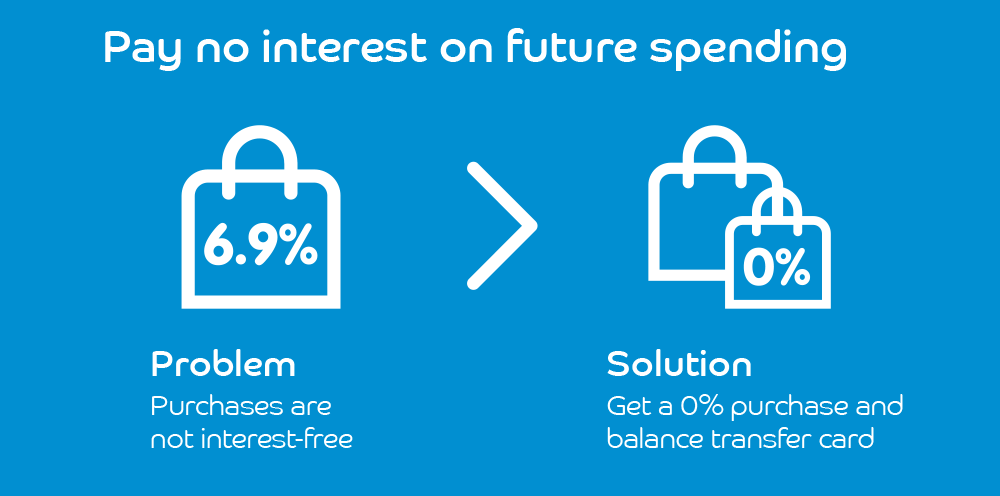

The 0% interest applies to all balance transfers you make to the account whilst you’re within the offer timeframe. But remember, interest rates may be charged on any purchases you make unless you have a balance transfer and purchase card with the same offer period, just check your offer for more details.

To fully benefit from a balance transfer, try and clear what you owe before the interest-free period ends, because after this time the card’s higher annual percentage rate (APR) will be applied to any remaining debt left on the account. You should always make at least the minimum repayments on time, otherwise you’ll incur a fee and/or lose the 0% interest offer on the balance transfer.

Try our Repayment Calculator to see how much you could save in time and interest by paying more than the minimum each month. This is especially useful if you don’t manage to clear the full balance before the 0% interest promotional period ends.

If you can afford it, pay off more than the minimum amount each month and you’ll bring your balance down more quickly.

If you have a large outstanding balance, even low interest rates can be costly. Move all the debt you can to a balance transfer credit card.

The amount you can transfer can vary, depending on your individual credit limit and the existing balance on your Barclaycard.

Transferring your balance will mean the same payments you were making will more effectively pay off a large credit card bill. By reducing, if not eliminating, your balance during the promotional period, you’ll be able to lower it with repayments that are affordable to you.

We’ll let you know the maximum amount you can transfer if your application is successful.

It can be tricky to manage repayments across multiple credit or store card accounts. If you choose to move the balance, watch out for any balance transfer fees. A one-off fee may apply for each balance transfer you make, so don’t forget to combine the cost of consolidating all your debts when finding the best balance transfer credit card. Our article How do I find the best balance transfer card? explains more.

Balance transfers help manage existing debt, but you might still pay interest on future purchases. That is unless you get a balance transfer credit card that includes 0% interest on purchases. Keep an eye on when the interest-free periods end, as the 0% interest on purchases may not last as long as the 0% interest period on your balance transfer.

If you don’t have a 0% interest purchase offer included in your balance transfers deal, think about whether it’s worth avoiding using the card for purchases. Your repayments could be used to pay these off first, delaying your balance transfer repayment. The key here is to make sure other purchases don’t prevent you from paying off the balance you transferred before your interest-free period ends.

Before following the steps below, it pays to do a review of your current credit card balances and the interest rates. That way, you’ll be able to decide which balance transfer card is best suited to your needs.

1. Choose the balance transfer card that’s right for you – not all balance transfer cards are the same. So take the time to compare how long the introductory periods are, and how much you’ll have to pay in transfer fees. You can compare our balance transfer offers to find the best card for you.

2. Apply for a Barclaycard online – by using our eligibility checker, you can find out if you’re likely to be approved before you apply.

3. Request the balance transfer – you can choose how much to transfer when you apply or once you’ve been approved. It’s up to you. If approved, you’ll have 60 days to transfer your old balance to your new account if you have chosen a balance transfer card from us. If you don’t complete the balance transfer, your promotional offer will expire.

To help manage your account and payments, you can download our Barclaycard app* and set up timely Alerts to help keep you in control of upcoming payments and your current balance.

*You need to be 16 or over to use the app. T&C’s apply.

It’s also a good idea to put together a budget and stick to it to avoid getting into more debt in the future.

Share this article