What is the use of a credit card?

How do credit cards work

Credit cards and ‘APR’ go hand-in-hand. But what does this famous three-letter term actually mean, apart from ‘Annual Percentage Rate’? Put simply, credit card APR is the total cost of borrowing over a year, including interest and standard fees. But by understanding a bit more about APRs, you can find they’re a quick way to compare credit cards, as well as figure out the total cost of using one.

APRs allow you to compare different credit cards more easily. That’s because the APR for every credit card on the market is calculated the same way, using the same credit limits and amounts of spending. APRs are all based on a credit limit of £1,200. On top of that, they always assume you spend the full £1,200 on the first day and then pay it back in equal, regular instalments over a year without any further spending. Finally, APRs don’t consider any other interest you may be incurring on your card.

That way, you can compare different APRs and know they’re measured the same way. This could help to make finding the right card much easier – particularly given the wide range of credit cards to choose from, and the different ways fees and interest rates are advertised.

Aside from the money you spend with a credit card, the main cost of using your card is usually the interest you’re charged on what you borrow. So if you pay off your balance every month by the due date, you won’t have to pay any interest.

However, if you make a purchase and don’t pay it off by the due date, then it’s added to your balance and you have to pay interest on it. So if you spend £500 in a month and don’t pay it off by the due date, you’ll be charged interest on that £500 the next month (if you’re not in a 0% promotional period).

And if you already have an existing balance from previous months that wasn’t paid off, this new spending will be added to that balance. Each month, you have to make a minimum payment on the due date, as well as interest on whatever outstanding balance still remains. So if you pay off your balance in full before the next payment due date, there’s no interest to pay. However, if you still owe a balance after your due date, interest is added to the amount you need to repay.

When borrowing on a credit card, you owe the outstanding balance, plus a percentage charged on top. This percentage, called the interest rate, is set by the lender when you sign up for the card.

For example, let’s say your credit card has an interest rate of 20%. If you borrow £1,000 in January and don’t repay it until the end of the year, the cost of borrowing would be 20% of £1,000, or £200. In reality, the actual cost could be higher because of compound interest (interest charged on interest) and other charges and fees.

This is just an example to make APR easier to understand – remember that you should make regular repayments throughout the year to manage your balance. Paying your balance off each month will affect the amount of interest you pay over the year.

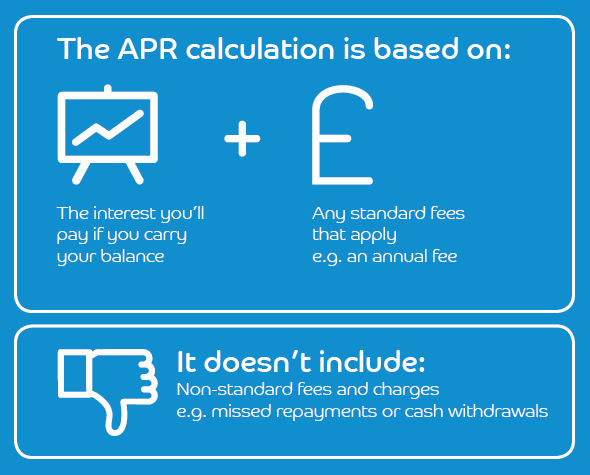

A credit card’s APR (annual percentage rate) is the total cost of its interest rate (e.g. 20%) plus the fees every cardholder pays as standard, such as the annual fee – it’s the cost of borrowing money over a year. All other fees and charges, such as for missed repayments and cash withdrawals are excluded from the APR.

The APR is based on the interest you'll pay if you carry your balance, as well as any standard fees such as annual fees that apply to your account. It doesn't include non-standard fees and charges (e.g. missed repayments or cash withdrawals).

APRs can be very helpful for comparing the cost of different credit cards, because they give you a good idea of how much different credit cards will cost compared to one another. That’s because the APR for all credit cards are calculated the same way. They’re based on the same amount of spending and consider the same kinds of fees. That way, you can use the APRs of different cards to compare what each card would cost the most. So the higher the APR, the more you’ll pay.

It’s worth knowing that when credit card providers give an APR for one of their cards, it’s based on an assumed credit limit. So when you see a representative example for any credit card, the APR is always based on how much it could cost if you borrowed £1,200 in a year. So the representative example and APR help you compare different products. Just remember that you might not be offered the same limit when applying, since that will be based on your financial history.

The APR is also based on the type of interest rate that applies to the way most people use the card. This is usually the Standard Purchase Rate, because most people use credit cards to make purchases. If you use the card in other ways, such as to transfer money or make cash withdrawals, different rates to the advertised APR could apply.

Now you know a bit about APR, you might be itching to bag the card with the lowest rate. But before you start comparing cards, it’s worth knowing the difference between representative APR and personal APR.

Representative APR is the rate given to at least 51% of the people who are granted the card by the credit card company, while personal APR is the rate you’re offered based on your personal circumstances. When a list of different credit cards is sorted from high to low by their APRs, you’re seeing what cards have the highest and lowest rates for the majority of people who get them. The cards aren’t necessarily ordered by those that will personally give you the highest or lowest APR.

You’ll know what APR you can get after you’ve applied. If it’s different to what you saw advertised as the representative APR, then you’ll know you’ve been given a rate based on your personal situation.

The APR you’re offered is decided by the credit card company when you apply and is based on your credit rating, how good you are at managing your money, and the amount you want to borrow. After applying for a credit card, you could find that your personal APR is higher, lower or the same as the representative APR.

Although they’re unlikely to ever come up in a pub quiz, here are a few other facts about APR worth knowing:

As long as you pay your credit card bill in full on time each month, you won’t have to worry about how high or low your APR is, as you won’t pay any interest. Also, some cards have higher or lower APRs because they’re designed for certain uses.

For example, credit cards designed to help build credit ratings tend to have lower credit limits and higher APRs because they’re aimed at people who don’t have a track record of making repayments. Certain rewards cards have higher APRs too, but they come with benefits, such as loyalty points and air miles, that can make the higher interest rate worth it for some people.

Barclaycard has a range of credit cards you can check out to find the best one for your needs.

Until now, the APR we’ve been talking about is the purchase APR – the amount of interest you pay on purchases.

But depending on the type of card you have, there may be other interest charges and APRs to consider:

Understanding APR is important – but there are other things to keep in mind.

If you don’t pay off your outstanding balance every month, charges and fees associated can increase the cost of borrowing. That’s because you’ll have to pay interest on the interest – which is called ‘compound interest’. This compounding effect isn’t included in the APR, and could make the cost of borrowing higher than you might think.

Finding out your personal APR is a bit like shaking a Magic 8-ball. You don’t know what rate you’ll be offered until you apply for a credit card, and because applying can be recorded in your credit history, it’s worth reading the eligibility requirements for the card before applying. You can also use our eligibility checker, which can give you an idea of whether you’re likely to be accepted. This type of ‘soft search’ isn’t recorded in your credit history and therefore won’t affect your credit rating.

If you already have a credit card with an APR that’s adding interest to your bill each month, you could consider moving the balance to a new card with a 0% interest promotional period.

Taking interest out of the picture for a while can make clearing the balance easier, as long as you’re confident you can pay it all off before the 0% interest period is over and APR kicks in again. Be sure to check if there are any transfer fees involved when you look at balance transfer card.

Here’s how the APR on a credit card could make a difference to how much you pay while clearing an outstanding balance, compared to the saving you could make if you transferred it to a card with a 0% interest period.

Imagine you have an outstanding balance of £1,200 on a credit card with 19.9% APR. If you kept the balance on that card and repaid £100 per month, it could take 1 year 2 months to clear it and cost £135 in interest payments.

As a comparison, if the balance of £1,200 was moved to a balance transfer card with a 30-month interest-free period and a 0.5% transfer fee, and you repaid £100 each month, the balance could be cleared in 12 months, with no interest and £6 in fees.

APR can sometimes seem like a tricky maths problem based on confusing percentages, rates and balances. Actually, it’s just about understanding the basics of interest and fees.

Now you know all the important bits, you can start comparing credit cards on a like-for-like basis.

Share this article